An insurance premium is an amount that an organization pays on behalf of its employees and the policies that a business has rendered. The expense, unexpired and prepaid, is reported in the books of accounts under current assets. Each month, the business’s accounting department would make an adjusting journal entry of $1,000, representing the amount of one month’s premium payment in the general ledger. It would be entered as a credit in the asset account and as a debit to the insurance expense account. When a company pays its insurance payments in advance, it makes a debit entry to its prepaid insurance asset account.

Risk mitigation

The current ratio is a useful liquidity metric to evaluate whether a company can meet its short-term obligations by utilizing assets which can quickly be converted into cash. The current ratio is calculated by dividing current assets by current liabilities. By definition, current prepaid assets would be included in the numerator, or current assets portion of the current ratio, and positively affect the results. Typically an entity will pay its insurance premiums at the beginning of the policy period, recognizing a prepaid asset subsequently amortized over the term of the policy. Therefore under the accrual accounting model an entity only recognizes an expense on the income statement once the good or service purchased has been delivered or used. Prior to consumption of the good or service, the entity has an asset because they exchanged cash for the right to a good or service at some time in the future.

Create a Free Account and Ask Any Financial Question

Common examples include rent, insurance, leased equipment, advertising, legal retainers, and estimated taxes. In business, prepaid expenses are recorded as assets on the balance sheet because they represent future benefits, but they are expensed at the time when those benefits are realized. It is usually listed together with other prepaid expenses and short-term assets. As the coverage period runs out, portions of prepaid insurance are expensed, and gradually the prepaid amount decreases to its complete use or expiration date. Although being a simple concept, it is important for an organization to correctly account for and recognize prepaid expenses on its balance sheet. Prepaid assets typically fall in the current asset bucket and therefore impact key financial ratios.

Prepaid Expenses

- Prepaid assets are nonmonetary assets whose benefits affect more than one accounting period.

- In this scenario, we would record a prepaid asset at the beginning of the contract and the expense of the subscription would be realized over the course of the year.

- On 1 September 2019, Mr. John bought a motor car and got it insured for one year, paying $4,800 as a premium.

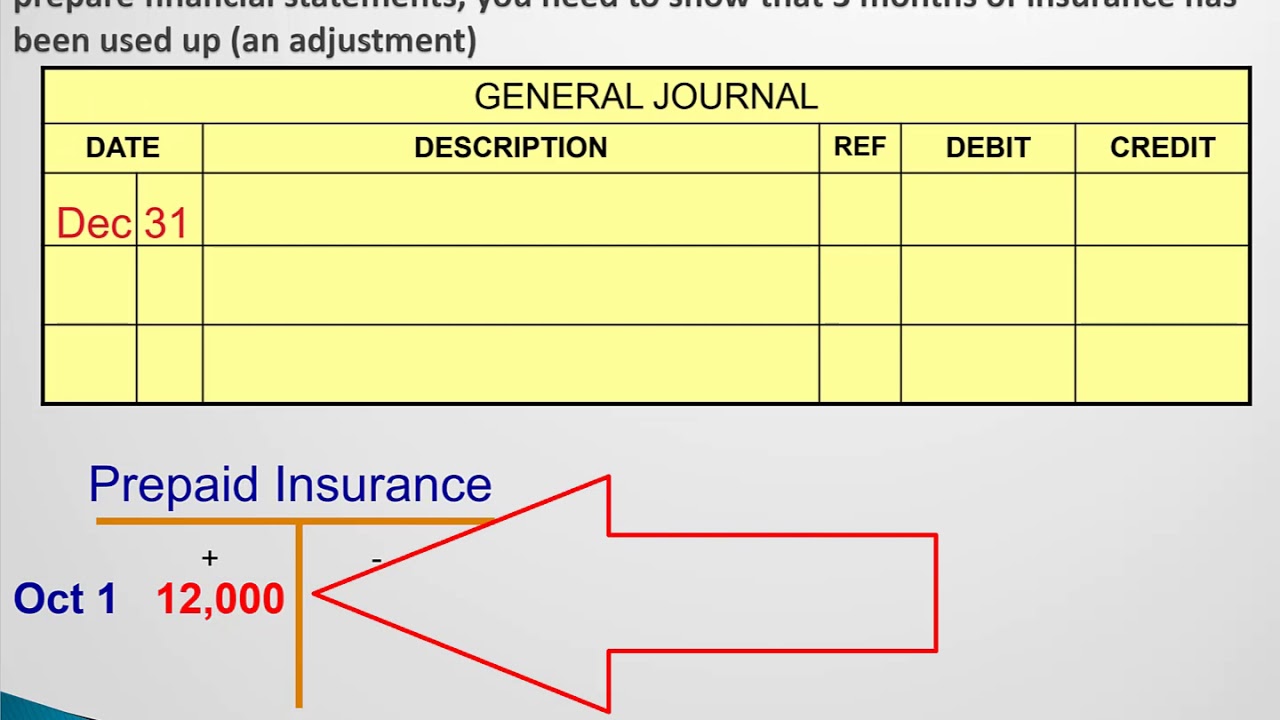

In this way, prepaid insurance has economic value, not unlike an investment in stocks or bonds, that can be redeemed at a later time. The company can record the prepaid insurance with the journal entry of debiting the prepaid insurance account and crediting the cash account. Each month, an adjusting entry will be made to expense $10,000 (1/12 of the prepaid amount) to the income statement is prepaid insurance a contra asset through a credit to prepaid insurance and a debit to insurance expense. In the 12th month, the final $10,000 will be fully expensed and the prepaid account will be zero. Journal entries that recognize expenses related to previously recorded prepaid expenses are called adjusting entries. They do not record new business transactions but simply adjust previously recorded transactions.

Which of these is most important for your financial advisor to have?

Prepaid insurance is usually considered a current asset, as it becomes converted to cash or used within a fairly short time. But if a prepaid expense is not consumed within the year after payment, it becomes a long-term asset, which is not a very common occurrence. The payment of the insurance expense is similar to money in the bank—as that money is used up, it is withdrawn from the account in each month or accounting period. Prepaid insurance for businesses is very valuable in terms of providing financial stability, budgeting accuracy, and risk mitigation. However, to ensure accuracy of financial statements, it is essential that these are recorded in the correct accounting period. By leveraging HighRadius’ Record to Report (R2R) suite organizations can automate prepaid insurance journal entry management, reducing manual errors and enhancing efficiency.

For example, if a company pays $12,000 for an annual insurance coverage, their monthly prepaid insurance expense is $1,000 ($12,000/12 months). This method guarantees that expenses are accurately allocated during the prepaid period, reflecting the steady utilization of insurance coverage. Prepaid insurance is nearly always classified as a current asset on the balance sheet, since the term of the related insurance contract that has been prepaid is usually for a period of one year or less.

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

Company ABC will initially book the full $120,000 as a debit to prepaid insurance, an asset on the balance sheet, and a credit to cash. To illustrate prepaid insurance, let’s assume that on November 20 a company pays an insurance premium of $2,400 for insurance protection during the six-month period of December 1 through May 31. On November 20, the payment is entered with a debit of $2,400 to Prepaid Insurance and a credit of $2,400 to Cash.

The company should not record the advance payment as the insurance expense immediately. This is due to, under the accrual basis of accounting, the expense should only be recorded when it occurs. Prepaid expense is an accounting line item on a company’s balance sheet that refers to goods and services that have been paid for but not yet incurred. Recording prepaid expenses must be done correctly and according to accounting standards. They are first recorded as an asset and then, over time, expensed onto the income statement. For example, assume Company ABC purchases insurance for the upcoming 12-month period.